Organisations use the Balanced Scorecard (BSC) to improve performance by combining financial and strategic metrics. It offers a holistic view of performance, linking operational actions to long-term goals.

The Balanced Scorecard was introduced by Robert S. Kaplan and David P. Norton in the early 1990s. It revolutionised performance measurement by integrating financial indicators with other key performance areas such as customer satisfaction, internal processes, and learning and growth, thus providing a balanced view of organisational performance.

In this guide, we will cover how to create a balanced scorecard and a template, as well as its benefits and limitations.

Definition of a Balanced Scorecard

The Balanced Scorecard (BSC) is a strategic planning and management system used by organisations to align business activities with the vision and strategy of the organisation, improve internal and external communications, and monitor organisational performance against strategic goals.

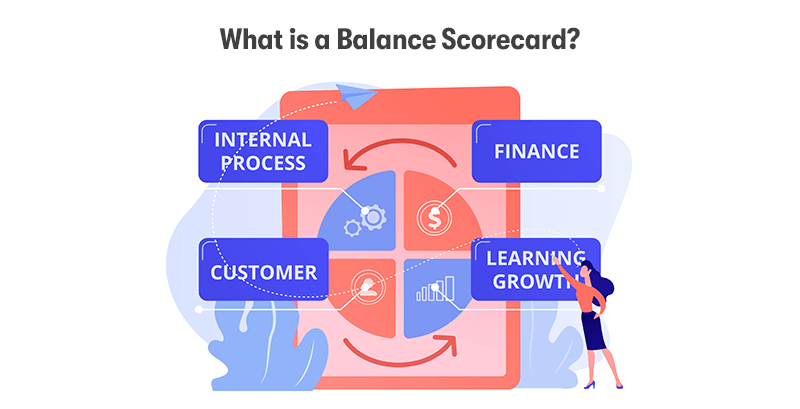

What is a Balance Scorecard?

The Balanced Scorecard provides a framework that includes performance measures and helps planners identify what should be done and measured. The Balanced Scorecard emphasises a balanced approach across four main perspectives:

- Financial Perspective

- Customer Perspective

- Internal Process Perspective

- Learning and Growth Perspective

The Balanced Scorecard helps organisations track financial outcomes and monitor the progress of building capabilities and acquiring the intangible assets they need for future growth. It acts as a comprehensive framework that translates a business's strategic objectives into a coherent set of performance measures that provide the foundation for a strategic management and execution system.

What are the 4 Components of a Balanced Scorecard?

The four components of a Balanced Scorecard, which represent different perspectives of an organisation's strategy, are:

Financial Perspective

This focuses on an organisation's financial objectives and enables managers to track financial success and shareholder value. It typically includes measures such as return on investment (ROI), revenue growth, profit margins, cash flow, and cost reduction.

Customer Perspective

This aspect concentrates on customer satisfaction and market share goals. Key performance indicators (KPIs) include customer satisfaction scores, customer retention rates, new customer acquisition, and market share in target segments.

Internal Process Perspective

This perspective examines the organisation's internal operational goals and focuses on the critical processes that enable it to satisfy customer and shareholder expectations. Measures can include process efficiency, cycle time, quality, and delivery performance.

Learning and Growth Perspective (or Innovation and Growth Perspective)

This component emphasises the intangible drivers of future success, such as human resources, organisational culture, information systems, and the ability to innovate and improve. KPIs include employee satisfaction and retention, skill set improvement, system availability and performance, and the rate of innovation in product or service offerings.

These components ensure that the Balanced Scorecard covers a broad spectrum of the organisation's performance, combining financial and non-financial measures. Doing so provides a more comprehensive view of how well an organisation is executing its strategy and achieving its vision.

Balance Scorecard Template

Creating a Balanced Scorecard template involves outlining the four key perspectives: Financial, Customer, Internal Process, and Learning & Growth. For each perspective, it's crucial to define strategic objectives, measures (or Key Performance Indicators - KPIs), targets, and initiatives that align with the organisation's overall strategy and goals. Here's a simplified template to get you started:

Financial Perspective

Objective: What you aim to achieve financially (e.g., Increase Revenue, Reduce Costs, Improve ROI)

Measures/KPIs: Metrics to track performance (e.g., Revenue Growth Rate, Operating Margins, ROI)

Targets: Specific goals for each measure (e.g., 10% revenue growth, 15% operating margin)

Initiatives: Projects or actions to achieve targets (e.g., Enter new markets, Cost reduction program)

Customer Perspective

Objective: Goals related to customers (e.g., Improve Customer Satisfaction, Increase Market Share)

Measures/KPIs: Metrics to assess customer-focused performance (e.g., Customer Satisfaction Score, Net Promoter Score, Market Share)

Targets: Specific goals for each measure (e.g., Score of 85 in Customer Satisfaction, 20% market share)

Initiatives: Actions to reach customer goals (e.g., Customer service training, Marketing campaigns)

Internal Process Perspective

Objective: What the company must excel at internally (e.g., Enhance Operational Efficiency, Improve Product Quality)

Measures/KPIs: Metrics for internal processes (e.g., Process Efficiency, Defect Rates)

Targets: Specific goals for each measure (e.g., 95% process efficiency, Reduce defect rate by 50%)

Initiatives: Actions to improve processes (e.g., Implement lean management, Quality control programs)

Learning & Growth Perspective

Objective: Goals for culture, people, and organisational capacity (e.g., Improve Employee Skills, Foster Innovation)

Measures/KPIs: Metrics for learning and growth (e.g., Employee Satisfaction, Number of New Patents)

Targets: Specific goals for each measure (e.g., Employee satisfaction score of 90, 5 new patents per year)

Initiatives: Projects to achieve these goals (e.g., Training and development programs, Innovation workshops)

This template serves as a starting point. Customise it according to your organisation's vision, strategy, and operational focus areas. Remember, the most effective Balanced Scorecards are those tailored to reflect an organisation's unique strategy and competitive environment.

Download our balanced scorecard template (word document).

Download our balanced scorecard template (PDF).

Balance Scorecard Method

The Balanced Scorecard method is designed to help organisations align their business activities with their vision and strategy. The methodology extends beyond traditional financial metrics to include broader perspectives that provide a more holistic view of organisational performance. Here is an overview of the BSC methodology's key components and processes:

Key Components

Financial Perspective: Focuses on measuring financial success and shareholder value.

Customer Perspective: Concentrates on customer satisfaction and market positioning.

Internal Process Perspective: Looks at internal operational efficiency and effectiveness.

Learning and Growth Perspective: Emphasises continuous improvement and innovation in workforce capabilities, information technology, and organisational culture.

Process Steps

Clarify Vision and Strategy: Start by clearly articulating the organisation's vision and strategic objectives. This ensures that the subsequent steps are aligned with the overall direction the organisation intends to take.

Translate Strategy into Objectives: Break the strategy down into specific, actionable objectives across the four BSC perspectives. This step involves translating high-level strategy into clear goals that can be communicated and acted upon.

Develop Measures and Targets: For each strategic objective, develop specific measures (or Key Performance Indicators - KPIs) that can be tracked over time. Set targets for each measure to provide a clear performance benchmark.

Select Strategic Initiatives: Identify and prioritise the projects and initiatives to help achieve the strategic objectives. This involves allocating resources to the activities that are expected to have the most significant impact on performance.

Implement and Monitor: Execute the strategic initiatives and regularly monitor performance using the developed measures. This step requires establishing a feedback loop where performance data is reviewed against targets to identify areas for improvement.

Adapt and Learn: Use the insights gained from performance monitoring to refine strategies, objectives, and initiatives. This continuous learning process is critical for adapting to changes in the external environment and ensuring long-term success.

Example of Balanced Scorecard

A Balanced Scorecard can help IT departments align their activities with the broader business goals, emphasising technical performance and how IT services contribute to customer satisfaction, internal process efficiency, and organisational growth. Here is an example of a balanced scorecard for an IT Service Management Department:

Financial Perspective

Objective: Reduce IT operational costs

Measures/KPIs: Cost reduction percentage, ROI on IT investments

Targets: 5% reduction in operational costs annually, 15% ROI on IT investments

Initiatives: Implement cloud-based solutions to reduce infrastructure costs, streamline IT procurement processes

Customer Perspective

Objective: Improve end-user satisfaction with IT services

Measures/KPIs: End-user satisfaction score, First call resolution rate

Targets: Achieve an end-user satisfaction score of 85% and, First call resolution rate of 90%

Initiatives: Develop a training program for service desk agents, upgrade IT service desk software for efficiency

Internal Process Perspective

Objective: Enhance IT service delivery efficiency

Measures/KPIs: Average incident resolution time, Change success rate

Targets: Reduce average incident resolution time by 25%, Achieve a 95% change success rate

Initiatives: Implement automated incident management tools, adopt ITIL framework for change management

Learning & Growth Perspective

Objective: Foster a culture of continuous improvement and innovation in the IT department

Measures/KPIs: Number of staff training hours, Number of innovation projects initiated

Targets: 40 training hours per IT staff per year, Launch 2 new innovation projects annually

Initiatives: Establish an ITSM training and certification program, Create an innovation lab for exploring new technologies

This example illustrates how an ITSM department can use a Balanced Scorecard to ensure its objectives and activities align with broader organisational goals. By focusing not only on financial and customer perspectives but also on internal processes and the growth and learning of its team, ITSM can demonstrate its value and contribute to the organisation's overall success.

The Advantages of a Balance Scorecard

The Balanced Scorecard approach offers several advantages to organisations seeking to improve their performance management and strategic execution. Here are some key benefits:

Aligns Strategy with Operational Activities

By translating an organisation's vision and strategy into a coherent set of performance measures, the BSC ensures that all parts of the organisation are working towards the same goals. This alignment enhances operational activities and strategic initiatives.

Provides a Comprehensive View

The BSC integrates financial measures with other key performance indicators related to customer satisfaction, internal processes, and learning and growth. This comprehensive view prevents organisations from focusing solely on short-term financial performance.

Improves Decision Making

With clear metrics for success across various aspects of the organisation, managers can make more informed decisions. The BSC provides a framework for balanced decision-making that considers multiple facets of organisational performance.

Enhances Communication and Focus

The Balanced Scorecard can help to clarify strategy and communicate it throughout the organisation. Linking individual performance to organisational goals helps employees understand how their work contributes to the company's strategic objectives, enhancing focus and motivation.

Facilitates Performance Measurement and Management

The BSC framework makes it easier to set targets and measure performance. By regularly reviewing performance data, organisations can manage by exception, focusing attention on areas that are not performing as expected.

Encourages Continuous Improvement

By monitoring performance across various areas, the BSC encourages organisations to continuously seek ways to improve processes, enhance customer satisfaction, and develop their workforce. This culture of continuous improvement can lead to sustained long-term success.

Supports Strategy Adjustment

The Balanced Scorecard allows organisations to adapt quickly to changes in the external environment. Regular strategic performance reviews can highlight when the strategy needs to be adjusted to meet changing market conditions or to capitalise on new opportunities.

Promotes Organisational Learning

Developing and implementing a Balanced Scorecard can promote learning within the organisation. It encourages a deeper understanding of strategic objectives, operational processes, and performance drivers.

Overall, the Balanced Scorecard is a powerful tool for strategic planning and management, helping organisations to achieve a balance between short-term performance and long-term strategic goals. It fosters a holistic approach to performance measurement and management, leading to enhanced strategic execution and organisational success.

Limitations of Balance Scorecards

While the Balanced Scorecard is a valuable tool for strategic management and performance measurement, it does have limitations and challenges. Understanding these can help organisations implement and use the BSC more effectively. Some of the critical limitations include:

Implementation Complexity

Developing and deploying a Balanced Scorecard can be complex and time-consuming. Organisations need to ensure they have clear strategies and objectives before translating these into measurable goals and metrics. This process often requires significant effort and buy-in from all levels of the organisation.

Requires Cultural Change

Organisations may need to undergo cultural changes for the BSC to be effective. Employees at all levels must understand and support the BSC, which can be challenging in organisations that are resistant to change or where there is a lack of communication.

Overemphasis on Measurement

There is a risk of focusing too much on the BSC's measurement aspects at the expense of dialogue and learning. Some organisations may become too fixated on tracking metrics and lose sight of the broader strategic objectives.

Data Overload

The BSC can lead to an overwhelming amount of data and metrics, making it difficult for managers to focus on what is most important. This can result in analysis paralysis, where decision-making is hindered by excessive information.

Risk of Misaligned Objectives

If not carefully designed, the objectives and metrics across the four perspectives of the BSC may not align well with each other or with the overall strategic goals. This misalignment can lead to efforts that do not contribute effectively to strategic objectives.

Static Framework

The business environment is dynamic, but the BSC can sometimes be too static, failing to adapt quickly to changes in market conditions, technology, or competitive landscapes. Organisations must regularly review and update their scorecards to ensure they remain relevant.

Quantification of Intangible Assets

Some aspects are difficult to quantify, especially from a learning and growth perspective. It can be challenging to meaningfully measure intangible assets like employee knowledge, skills, and morale.

Potential to Ignore External Factors

While the BSC focuses on internal performance measures, it can sometimes lead to organisations needing to pay more attention to external factors such as market trends, competition, and regulatory changes. It's important for organisations to complement the BSC with external environmental scanning.

Resource Intensive

Implementing and maintaining a BSC can be resource-intensive regarding time, money, and personnel. Smaller organisations, in particular, may find the costs and effort required prohibitive.

Understanding these limitations is crucial for organisations considering the Balanced Scorecard as a tool for strategic management. By acknowledging and addressing these challenges, organisations can leverage the BSC more effectively to achieve their strategic objectives.

Final Notes on Balanced Scorecard Example

In conclusion, the BSC fosters a holistic approach to strategic management by incorporating perspectives on financials, customers, internal processes, and learning and growth. However, its effectiveness has challenges, including the potential for complexity and the need for rigorous implementation and adaptation.

An example shows how the BSC can be applied to specific organisational contexts, demonstrating its versatility and potential to drive continuous improvement and strategic alignment.

Despite its limitations, the Balanced Scorecard remains a powerful tool for organisations seeking to navigate the complexities of modern business landscapes.

One final tip - regularly review and update your Balanced Scorecard to ensure it reflects current objectives and challenges, keeping your strategy dynamic and responsive.